Fintech is growing quickly in Indonesia, positioning the country as one of the most important drivers of fintech Asia. This is because more people are using digital payments, more people are getting access to financial services, and the government is very much in favor of a cashless economy.

As Southeast Asia’s largest economy, Indonesia is not just participating in regional innovation — it is actively shaping broader Asia finance trends, particularly in mobile payments and SME integration. Not many other markets in the area are as big as Indonesia.

Digital payments in Indonesia have gone from being a niche service to something that everyone does every day in the last ten years. New ideas in fintech are changing the way people in Indonesia save money, run their businesses, and grow them. For instance, people who live in the country can now use mobile banking, and street vendors can now take payments through QR codes.

These changes reflect not only domestic modernization but also deeper Asia economic growth, where digital finance is becoming central to productivity and regional trade. It’s no longer a question of if Indonesia will use digital finance, but how the change will affect the larger fintech asia ecosystem.

The Rise of Digital Payments in Indonesia

Indonesia has one of the fastest-growing digital payment systems in the ASEAN region. People have sent a lot more money through e-wallets, mobile banking apps, and QR-based systems in the last few years. Before you publish, make sure to look at the most recent data from Bank Indonesia.

There are a number of structural reasons for this rise:

- There are more people who use smartphones.

- Low-cost access to mobile internet

- A group of young people who have always used technology

- More and more people are shopping online.

- People are starting to trust digital financial services more and more.

People of all ages and backgrounds now use e-wallets. These days, drivers, food vendors, small stores, and even regular markets all accept payments made with QR codes.

This widespread use is helping Indonesia’s fintech industry grow, making it the clear leader within business Asia’s fintech market.

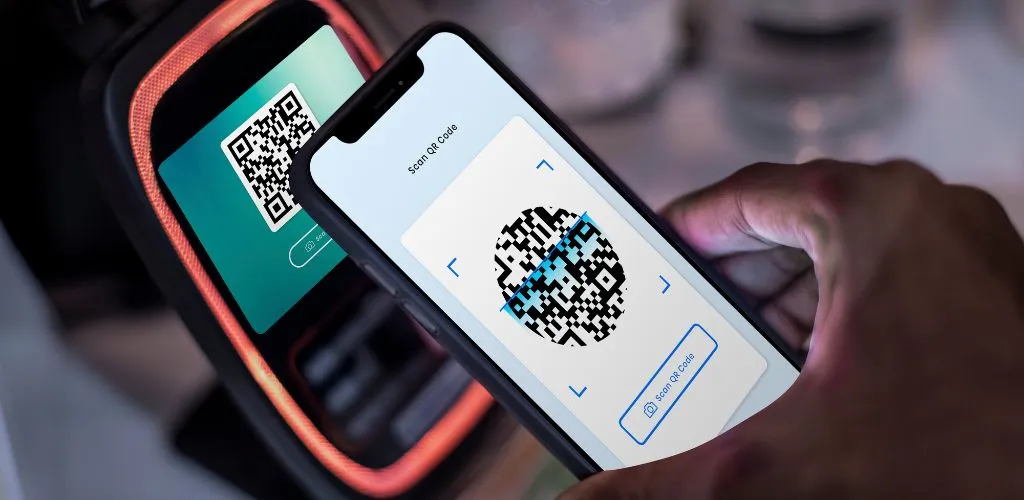

QRIS and the Standardization of Payments

The QRIS payment system (Quick Response Code Indonesian Standard) is one of the best things that has happened to Indonesia’s digital finance.

Bank Indonesia created QRIS to combine different QR payment systems into one standard system. Merchants no longer need to get separate QR codes for each service. You can now pay from a lot of apps with just one QRIS code.

This project has:

- Getting merchants on board faster

- Less trouble with how things work

- Costs for infrastructure went down.

- More openness and better tracking

These changes have helped a lot of small and medium-sized businesses (SMEs). Warungs, street vendors, and small stores can now be part of the digital economy without having to spend a lot of money.

More importantly, QRIS is becoming more compatible across ASEAN, which makes it easier to do business across borders. This means that Indonesia is not only a part of the integration of fintech in Asia, but also a key player in Asia finance trends.

E-Wallet Competition and Ecosystem Expansion

There is a lot of competition in Indonesia’s fintech scene, and it is always changing. A lot of digital banks, e-wallets, and super apps are trying to make their ecosystems bigger.

Due to competition, people enjoy using it more. There are promos and deals that cost less money, loyal customers can get cash back and rewards, and this mean of payment work along to ease people’s experiences with shopping, transportation, and food delivery services

As digital payments become more common, businesses in Indonesia are shifting their focus from rapid growth to making the ecosystem stronger. There are also surge in:

- Ways to help small and medium-sized business get money

- Pay Later services

- Micro-lending products

- Investment in digital ways

Fintech Asia has come a long way since it only handled payments. It now has a full range of financial services.

Fintech companies can try out models that work in Indonesia and then use them in other parts of Business Asia markets.

Financial Inclusion and Rural Penetration

One of the biggest effects of fintech’s growth in Indonesia is that it has made it easier for more people to get financial services.

A lot of people didn’t have bank accounts or the money they needed in them. Digital wallets and mobile banking are making things different.

Some of the big changes are:

- Easier to create an account

- Verifying someone’s digital identity

- Microfinance that works on phones and tablets first

- Providing government assistance through apps and websites

People in rural areas don’t have to go to the bank as often because they can pay online. People who own farms, run small businesses, or work for themselves can now send and receive money online.

This makes Indonesia’s economy stronger and helps Asia economic growth, as financial inclusion enables broader participation in formal economic systems

Small and medium-sized businesses also need to be a part of the financial system. Digital transaction records help small businesses build credit histories, which makes it easier for them to get formal loans.

The Role of SMEs in Driving Digital Payments

Small and medium-sized businesses (SMEs) are very important to Indonesia’s economy because they account for more than 61% of the country’s GDP. The changes in fintech asia have an even bigger effect because they use digital tools.

Here are some ways that digital payments can help small and medium-sized businesses (SMEs):

- Keep track of how much money you make in a clear way.

- Take out loans to pay for your working capital.

- Become online stores.

- Assist customers who are not in your area.

Connecting POS systems to e-wallets and banking applications is now possible, which makes running a company simpler. Small and medium-sized enterprises can’t just desire to become digital; they have to.

As more small and medium-sized firms (SMEs) join the digital ecosystem, Indonesia’s position as a hub for fintech Asia development becomes stronger.

Balance Between Regulatory Stability and Innovation

Digital payments are performing successfully in Indonesia since the laws don’t change.

The Financial Services Authority (OJK) and Bank Indonesia have plans for:

- Getting permission to use e-money

- Permits for digital banks

- Making sure consumers are safe

- How to follow the guidelines to keep your computer secure

Easy-to-understand rules protect both consumers and investment.

Regulatory control hasn’t prevented new ideas from coming up; in fact, it has contributed to healthy competition and long-term development. This balance makes Indonesia seem like a better area to conduct business in the Asian fintech sector. It also makes the contributions to Asia finance trends stronger.

Challenges in a Maturing Market

The digital payment sector in Indonesia is developing swiftly, however it still has several problems:

- Fintech companies are under pressure to earn money.

- More and more risks to cybersecurity

- Worries about protecting user data

- Consolidation due of tough competition

These are natural things that happen in a rising sector, and they don’t suggest that the industry isn’t solid.

Companies with long-term objectives are likely to gain stronger when the market gets smaller. This will assist Indonesia’s fintech Asia industry expand gradually.

The Important Role of Indonesia in Fintech Asia

Fintech Asia has a unique advantage in Indonesia because the country has a large market for its own products.

Indonesia has more than 270 million people, and the middle class is getting bigger. There is a lot of digital activity there, too. Indonesia acts as:

- A place to test out new ideas in financial technology

- There isn’t much of a market for investors in the area.

- A reason for ASEAN to add digital finance across borders

Cross-border QR payment interoperability projects show that the world’s economies are becoming more connected. As ASEAN moves toward digital economic integration, Indonesia’s payment system could be very important.

It’s not just that the country is following fintech trends; it’s making them happen.

What Will Happen to Digital Payments in Indonesia

There are a number of trends that are likely to affect the next step in Indonesia’s digital payments:

- AI helps find and mitigate fraud

- More services for online banking

- Transaction data helps small and medium-sized businesses make more money

- More QR payments between countries

- Fintech and online shopping collaborate together in depth

As the country’s digital infrastructure gets better, it’s likely that more people in smaller towns and cities will start using it as well.

Fintech Asia will care more and more about how well Indonesia can keep its economy stable while also encouraging new ideas.

Conclusion: Building a Stronger Cashless Economy

Changing to digital payments in Indonesia is more than just a change in technology. The economy is changing in terms of its structure.

Indonesia is a big part of fintech asia because e-wallets, the QRIS payment system, SME digital onboarding, and strong government support are all very common there.

Digital payments are now a normal part of the economy. They help businesses get started, make it easier for everyone to get financial services, and connect different areas.

As Indonesia’s financial system gets more modern, it will probably have an even bigger impact on fintech asia. Eventually, this will make it the leader in Southeast Asia’s digital economy.

Common Questions (FAQ)

Why is Indonesia important to fintech asia?

Indonesia has a lot of people, a strong small and medium-sized business (SME) sector, and people are quick to adopt new technologies. This is why Southeast Asia is one of the best places to use digital payments.

What is the QRIS payment system?

QRIS is Indonesia’s standard way to pay with QR codes. It lets different businesses that deal with digital payments work together.

What are the pros of digital payments for small and medium-sized businesses?

They make transactions more open, make it easier to get loans, lower the cost of doing business, and bring in more customers.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}